Market Update: Volatility falls but it’s still cloudy

The US Supreme Court just announced that cannot use the Emergency Powers Act to impose reciprocal tariffs. Stocks rose, US government bond prices fell somewhat, and the dollar weakened slightly. The moves are positive but not yet meaningful. Much will now depend on Trump’s likely attempts to reimpose tariffs by other means, the potential trade disruptions, and who might be eligible for tariff refunds.

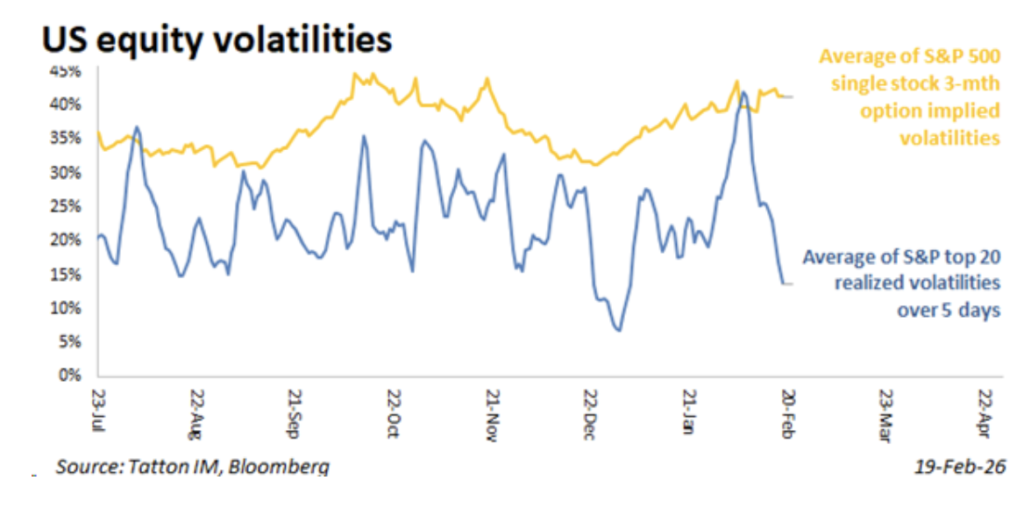

Markets were quiet up to that point. We wrote last Friday that individual stock-level volatility was significantly higher than index-level volatility, but stock-level volatility fell last week (chart below). Markets are still preoccupied with AI disruption and the underperformance of large cap stocks, relative to small cap, but selling pressures have dissipated, and the dollar bounced (before the tariff news) against most developed world currencies.

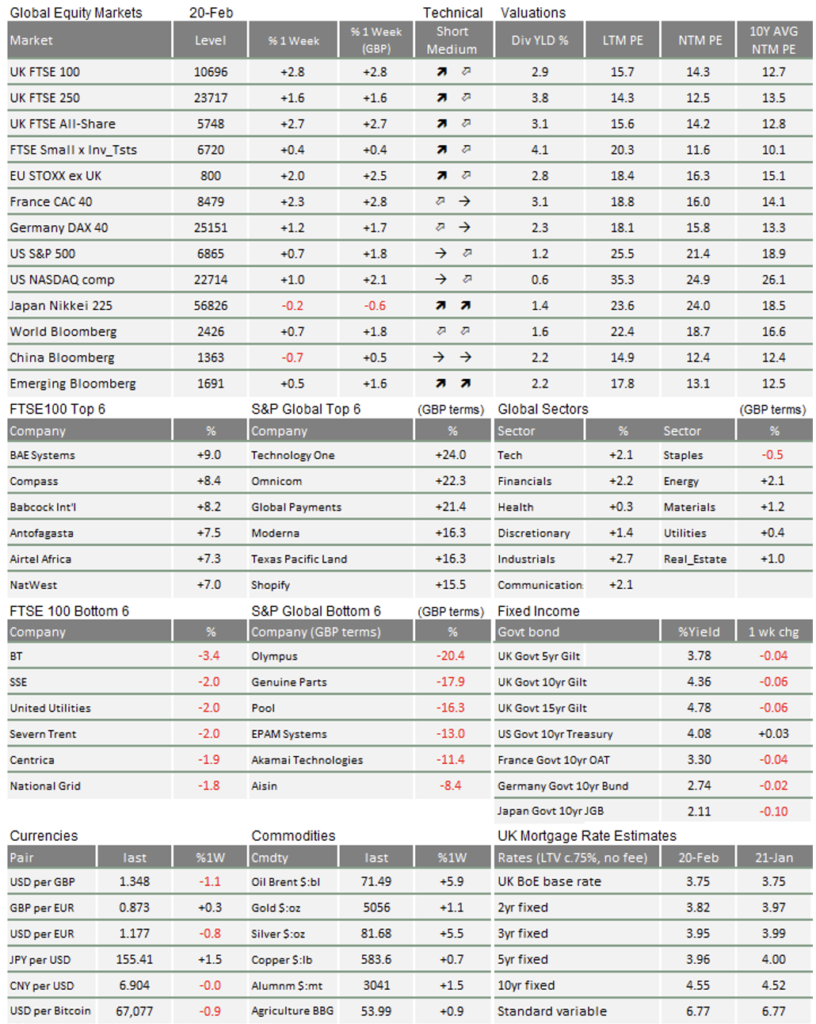

UK markets had a good week, thanks to a “Goldilocks” combination of economic data. January’s unemployment rate rose to 5.2% but that probably caused consumer price inflation to fall to 3% year-on year (from 3.4%). CPI will probably hit the 2% target next quarter, allowing an interest rate cut in March. Still, January’s retail sales were surprisingly robust and net tax receipts hit a record £30bn. No one likes being taxed more but international bond investors see it as evidence of fiscal discipline.

A calming base to build on, but AI capex is becoming a drag

Judging from high option prices, investors are still worried about stock volatility, but individual stock price swings are close to six-month lows. Microsoft and Amazon have been hurt by AI disruption stories, but their shares calmed down in the last few days. They still have not recovered, though, and there is no ‘buy the dip’ mentality.

That may not be a bad thing. Less stretched price-to-earnings valuations lay the ground for future gains. Unlike a few months ago, valuations are not being fuelled by market liquidity; stocks need stronger expected earnings growth to move ahead. The continued sell-off in cryptocurrencies and the rebounding dollar point to a market driven by fundamentals rather than speculation. That should be more stable.

US corporate earnings reports are okay, but some Q1 2026 forecasts have been downgraded. Tech firms are still spending big on AI infrastructure, but Absolute Strategy Research have pointed out that infrastructure costs are rising rapidly. Companies are committing more capital expenditures (capex) but not getting more from it. Capex inflation could prove to be a drag on future earnings.

This is not good news for the so-called AI ‘hyperscalers’, and it could reinforce the market rotation we have seen this year. The money stored up in big tech firms’ equity valuations is now being spent in the rest of the global economy. The recent strength of Asian chip manufacturers is testament to that.

Despite growing competition, Nvidia is a major beneficiary. The AI chipmaker will report its Q4 2025 results next Wednesday. CEO Jensen Huang will likely paint a rosy outlook for this year, given the AI industry’s continued capex.

Still unclear if AI is eating jobs

In the US, JP Morgan’s economists are forecasting strong 2026 US growth – while downgrading other regions – thanks to the wave of AI capex and looser fiscal policy. Upcoming tax rebates will help US consumers, but JP Morgan’s own nowcasts (an estimate current economic activity) are somewhat lower than their bullish predictions.

Uncertainty about the US economy is reflected in a split amongst the Federal Reserve’s voting committee. Hawkish members, led by chairman Powell, expect stronger consumption and inflation, fuelled by AI productivity gains. Dovish members either think those productivity gains will lower costs or raise unemployment. Stalling job numbers lead us to side with the doves, for now. We will have to watch the US household savings rate: consumers have been spending their savings, but might start tightening belts.

We still do not know whether AI is displacing jobs or not. Rising youth unemployment in the UK might suggest AI job losses, but you could also just explain that via higher costs for employers (minimum wage rises and employer NI). Falling youth unemployment in the US might be evidence against AI job losses, but that might be from tighter immigration. It is hard to untangle all these factors.

Get ready for more Trump disruption

Crude oil prices jumped 5% on Wednesday, after Russia trashed the slim hopes of a ceasefire with Ukraine. However, the major impetus comes from the US’s pressure on Iran. President Trump has signalled readiness to strike Iran, although the prospects of a drawn out conflict look remote. Trump favours short sharp ‘wins’ in his foreign interventions. He might even try to bomb all targets identified by his military in Iran while markets are closed over the weekend.

Geopolitics are driving oil markets in the short-term, but global oil supply is still rising faster than demand. OPEC+ is ramping up production, and the International Energy Agency (IEA) is forecasting weaker oil demand (though the IEA’s forecasts are lower than most others). All that to say, oil prices have room to fall if tensions calm.

It has been a while since Trump has been the centre of market attention. If his actions against Iran do not move markets, further tariffs might. Now that the Supreme Court has ruled against the president’s tariffs, he will look for other ways to implement them, like sector-specific ‘national security’ measures. Those might be more disruptive for global supply chains than the current regime.

In their dealings with the White House, many nations are pursuing “strategic under-implementation”, according to trade expert Sam Lowe. That means promising Trump what he wants and then stalling, but nations will have to cough up something eventually, as Japan is now experiencing. Tokyo unveiled the first tranche of its $550bn fealty pledge to Washington this week: a $36bn investment in US oil and gas. With new tariff looming and other nations strategically under-implementing, markets might get another episode of the Trump show soon.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.